The global private investment market showed signs of recovery in 2025 after three years of slowdown; however, this recovery did not signal a full return to the market’s previous peak, nor did it represent a continuation of the downturn seen from 2022 to 2024. Following the pressure caused by interest rate shocks and geopolitical uncertainty, deal value increased in some segments, exits became active again, and the IPO market gradually regained momentum. However, the simultaneous decline in deal count, fundraising, and liquidity shows that the market has not returned to its former boom cycle. Instead, it has entered a more selective and concentrated phase.

Overview of the Private Equity Industry

Fundraising remained subdued in 2025

According to Bain & Company’s private equity report, despite a partial recovery in dealmaking and exit activity, fundraising across private markets has yet to return to the boom levels seen in 2021 and 2022. After three consecutive years of decline, global fundraising for alternative assets stabilized in 2025, remaining at around $1.3 trillion.[1]

| The state of private equity in 2025 compared to 2024 | |

| Total value of PE transactions worldwide | 19% |

| Total value of PE transactions in Asia | -5% |

| Number of PE transactions worldwide | -9% |

| Number of PE transactions in Asia | -10% |

These figures provide a broad view of the global Private Equity market, covering Buyout, Growth, and Venture Capital. In 2025, the market improved in terms of deal value, while deal count continued to decline. In other words, capital became increasingly concentrated in fewer, larger, and more selective opportunities. Investment activity was lower in volume, but more targeted in nature.

Globally, PE-backed exit value grew by more than 40% in 2025, supported largely by the return of IPO activity and an almost 100% increase in the number of PE-backed exits through public listings. At the same time, megadeals—transactions valued above $2.5 billion—regained momentum. A notable example was the announced $55 billion take-private acquisition of Electronic Arts, the largest PE deal on record. In addition, 2025 ranked as the third-largest year in history for take-private transactions, either by deal count or deal value.

In Asia, the market picture was weaker. In 2025, PE deal value declined by around 5%, while deal count fell by 10%. Although PE-backed exit value in Asia increased by 28%, the number of exits dropped by 8%. This suggests that the overall increase in exit value was driven by a limited number of larger exits, while the exit path remains constrained for a broad base of portfolio companies—a continued concern for LPs.[2]

Within the region, Japan once again stood out, recording growth in both deal value and deal count. China also posted double-digit growth in deal count, supported by improved policy visibility and stronger market sentiment.[3]

The Global Venture Capital Landscape

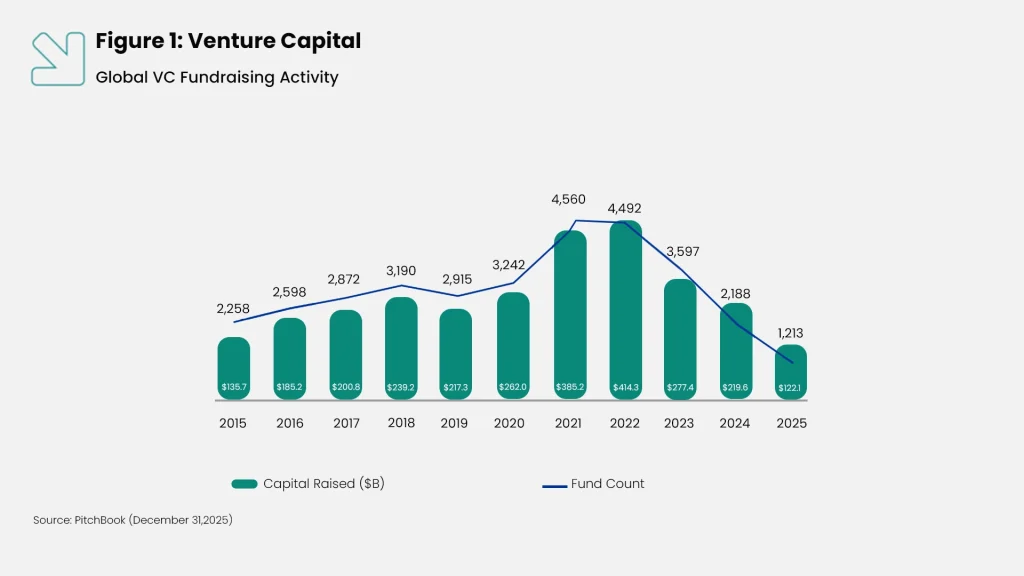

The global Venture Capital market remains under pressure, with capital becoming increasingly concentrated. Even the largest funds are facing fundraising challenges. The top 10 VC funds raised only $26.7 billion in new capital commitments in total—the lowest level since 2019 and 35% below 2024.

The main drivers behind this trend are the prolonged weakness in liquidity, limited exit opportunities, and LPs’ growing preference for lower-risk strategies.

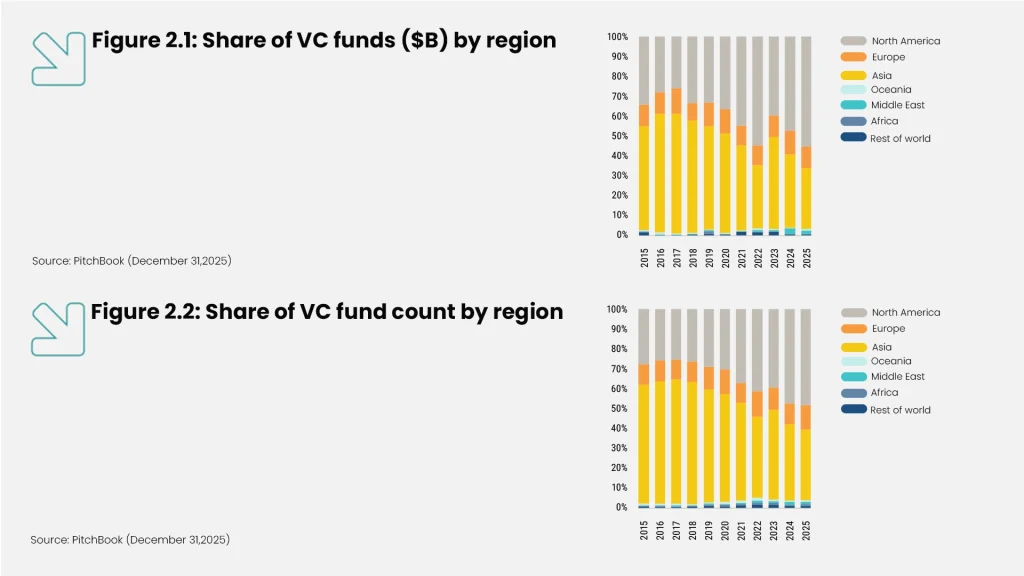

In 2025, VC fundraising shifted even more clearly toward more mature markets. North America captured 55.3% of new capital commitments, reaching its highest share since 2008. Europe also managed to preserve part of its historical share, although the overall volume of commitments declined.

By contrast, Asian VC funds accounted for 30.6% of total commitments—their lowest share since 2012. Weak liquidity in markets such as Southeast Asia and India reduced some of the global investor appetite that had built up during the low-interest-rate era.

As a result, capital increasingly flowed toward ecosystems with deeper VC infrastructure, longer-standing relationships with LPs, and more reliable exit pathways. After a period of sharp valuation growth, the VC market has now entered a phase of recalibration. LPs have become more selective, exits have slowed, and capital is increasingly moving toward funds with stronger track records, more credible brands, and clearer paths to capital return.[4]

| The state of private equity in 2025 compared to 2024 | |

| Total value of PE transactions worldwide | 27% |

| Total value of PE transactions in Asia | -11% |

| Number of PE transactions worldwide | -10% |

| Number of PE transactions in Asia | -11% |

This table presents a mixed picture of the global Venture Capital market in 2025. On the one hand, VC deal value grew by around 27%, while one-year IRR reached 12%—a sign of improvement compared with the difficult market conditions of 2022 and 2023. On the other hand, deal count declined by 10%, and VC fundraising remained under pressure, falling by 33%. In other words, global VC has moved away from a full downturn, but it continues to face liquidity constraints, lower deal activity, and cautious LP sentiment.

Global VC in 2025 was no longer in a deep slump, but it had not yet entered a broad-based recovery. Market growth was mainly visible in dollar value and in larger, more concentrated deals—not in deal volume or fund formation. As a result, fundraising remains challenging for startups, while VC funds increasingly need to demonstrate liquidity, successful exits, and realized returns to rebuild LP confidence.

In Asia, the picture was weaker. VC deal value declined by around 11% in 2025. Although this was less severe than the 17% decline recorded in 2024, the market remained in negative territory. Deal count also fell by 11%, suggesting that market pressure was not limited to a few large transactions. Instead, the broader flow of venture investment across Asia has been affected by more cautious investor behavior.[5]

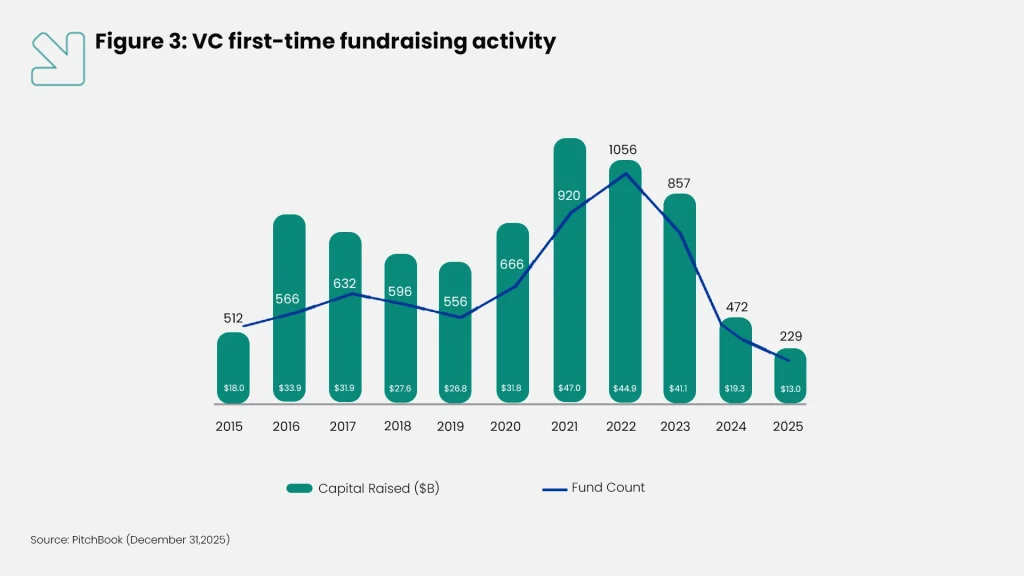

Figure 3 shows that the market has become significantly more challenging for first-time managers. The number of VC funds raising capital for the first time declined from 1,056 funds in 2022 to only 229 funds in 2025. This sharp drop indicates that, under current market conditions, LPs are less willing to take risk on new managers and are allocating more of their capital to experienced fund managers with established track records.[6]

However, this environment can create opportunities for CVCs. As traditional VC firms become more cautious, CVCs with available capital, strategic patience, and industry access can enter attractive opportunities with greater selectivity.

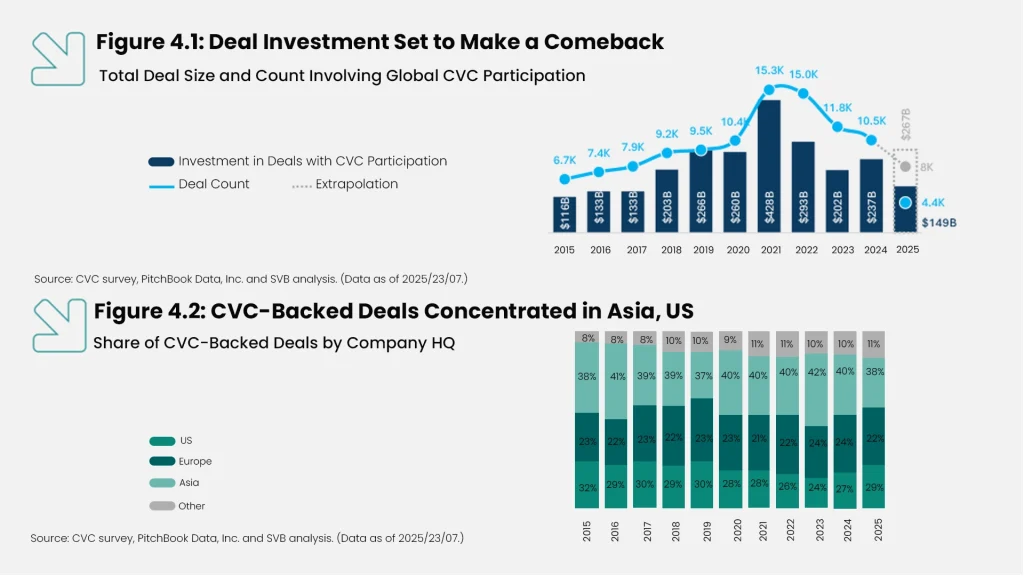

Total Deal Value and Deal Count with Global CVC Participation

In 2025, both the number of deals and the total investment value of transactions involving CVC participation improved compared with the market low of 2023. However, deal count remained below the peak levels seen in 2021 and 2022.

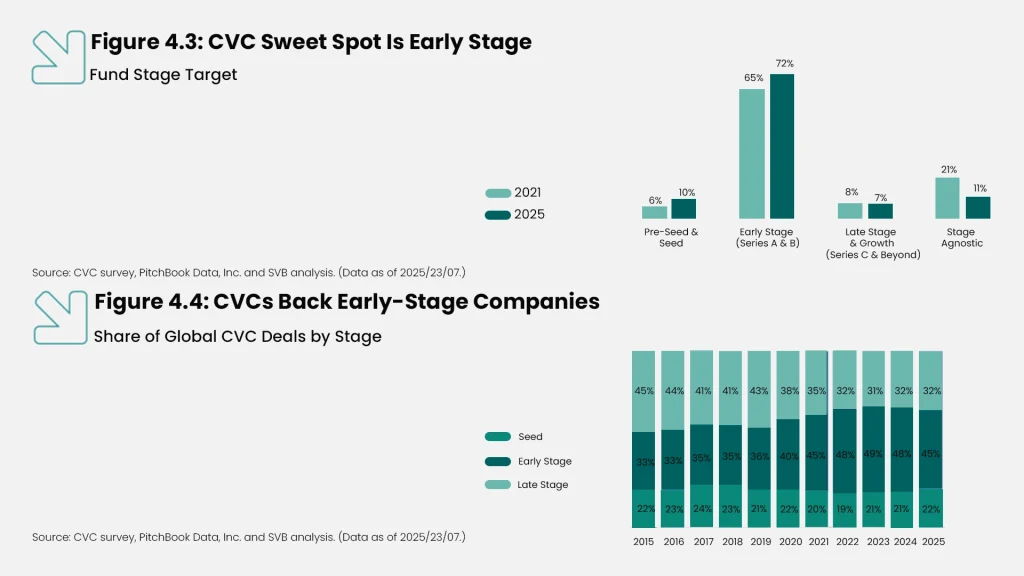

The share of Seed and Early-stage deals in total CVC activity reached 67%, compared with around 55% in 2015. This trend suggests that CVCs are no longer entering only at the growth stage or in larger funding rounds. Instead, they are engaging with startups earlier in their journey to gain access to better opportunities and create greater room for strategic influence.

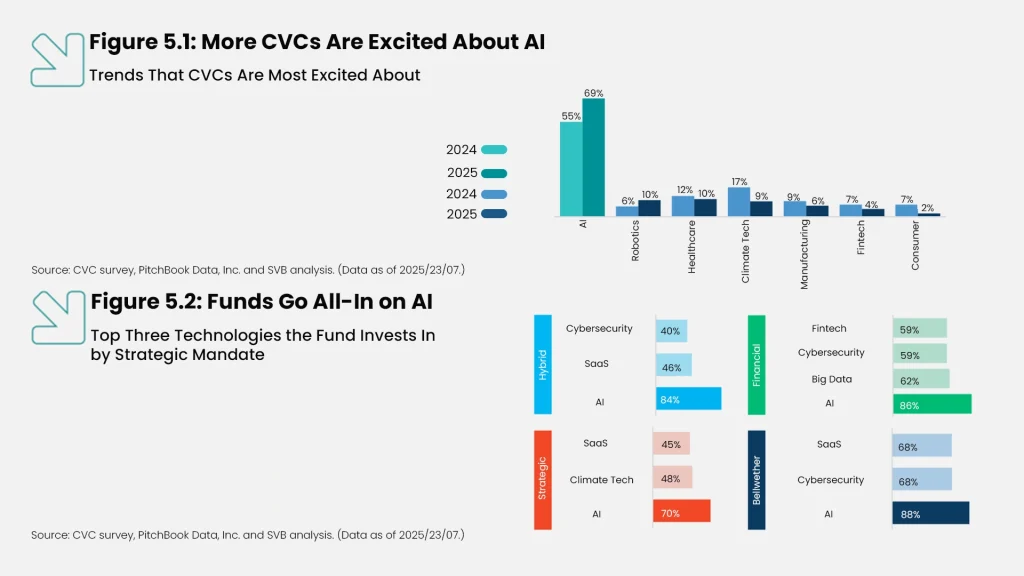

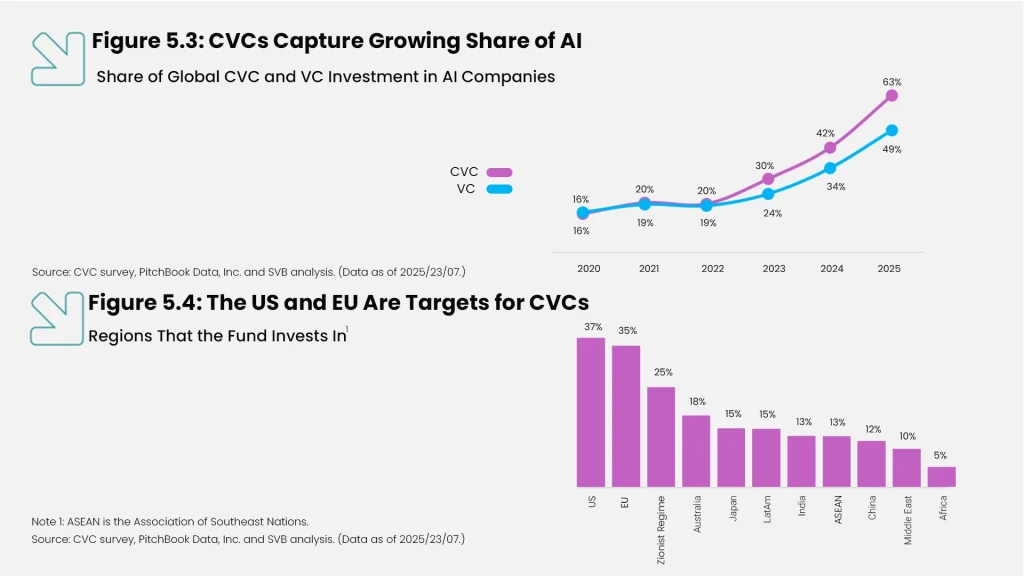

AI Became a Central Focus for CVC Activity in 2025

Artificial Intelligence became a central focus of CVC activity in 2025. According to the CVC Survey by PitchBook Data, Inc., 69% of respondents identified AI as the most attractive investment trend, up from 55% in 2024.

This concentration is also visible in deal activity. In 2025, for every dollar invested by CVCs, 63 cents went to AI companies, compared with 49 cents for traditional VC investors. This trend shows that, for many CVCs, AI is no longer merely an experimental investment area. It has become part of the core of their portfolio strategy.[7]

Expectations for 2026

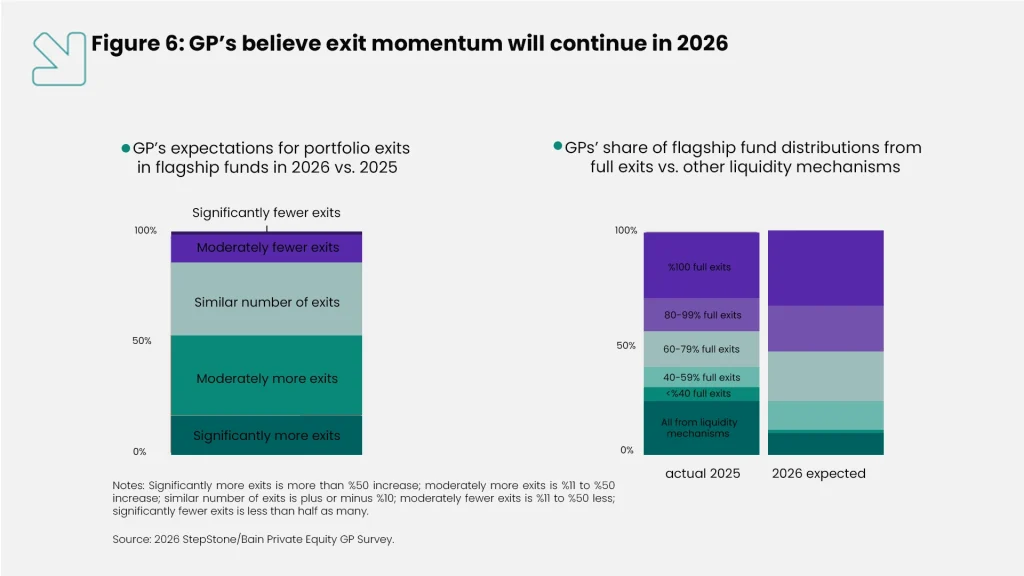

The outlook for 2026 appears more optimistic. Although unexpected events—or so-called Black Swan events—have made market forecasting more difficult in recent years, conditions for stronger dealmaking and exit activity are improving, provided that no major new shock emerges.

According to the StepStone/Bain Private Equity GP Survey 2026, improving market conditions have strengthened GP confidence. The majority of GPs expect to complete more exits in 2026 and rely less on alternative liquidity mechanisms to return capital to LPs.[8]

The Private Equity industry has reached an inflection point. In the 2026 market, competition is no longer defined only by access to capital or the ability to execute large transactions. It increasingly depends on GPs’ ability to create real value, drive rapid and sustainable EBITDA growth across portfolio companies, manage liquidity, and return capital to investors in a timely manner.

Today, LPs are paying closer attention to funds with strategies that are clear, repeatable, and easy to explain. They are looking for managers that can demonstrate, through tangible evidence, how they create value, how they exit investments, and how they return capital to their investors.